Costs for contribution margins

We have defined three groups for the calculation of your contribution margin, so that you can follow the result in three stages, depending on your interest.

In classic contribution margin accounting, the cost of goods sold and personnel costs are taken into account. If you maintain the purchase prices in the item master, the cost of goods is calculated much more accurately. An additional calculation here is then omitted, or takes place only additionally flat-rate. Alternatively, you can enter a revenue-dependent flat-rate cost of goods here.

Personnel costs are also recorded much more accurately using time recording or even absolutely accurately using the web interface interface to the payroll office. Alternatively, you can enter a flat rate depending on turnover or, in the case of fixed salaries, even the fixed costs.

The cost of goods sold (when using groupplanning) and the personnel costs (when using personnel costplanning) are always taken into account in DBI.

For all other costs use up to three groups, called DBI, DBII and DBIII (DB=contribution margin).

The multi-level contribution margin calculation helps you to further split the costs and offers you a subtotal for consideration after each group DBI to DBIII.

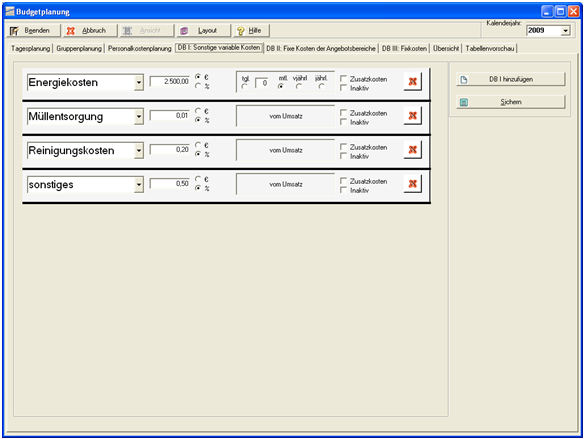

There is generally no fixed rule which costs you put into which group. We give you some direction here for guidance. You can create a new position using the Add to DBI button. Specify the name and type of calculation and choose Save to complete.

Example DBI - Variable Costs

The DBI area lists the variable costs (costs that you can influence).

In our example, monthly energy costs have been fixed at €2,500. Cleaning costs, for example, account for 0.2% of sales. It is recommended to combine several small positions in Miscellaneous.

Example DBII - Fixed Costs

In most cases, you cannot influence the fixed costs.

In our example, we have set up the rent at a fixed rate of €6,000 per month, but the ancillary rental costs are linked to the turnover.

Example DBIII - Fixed costs

Use this area for fixed costs that you do not want to assign to the other two areas. For example, participation in advertising associations, franchise fees and others.

Back to the overarching topic: Set Up Budget Planning